By clicking “Accept All Cookies”, you agree to the storing of cookies on your device to enhance site navigation, analyze site usage and assist in our marketing efforts.

By clicking “Accept All Cookies”, you agree to the storing of cookies on your device to enhance site navigation, analyze site usage and assist in our marketing efforts.

Why Arbitrage Opportunities Fail Even When Prices Are Right

And How Intelligent Arbitrage Detection Systems Are Transforming Execution in Energy Trading

Arbitrage appears simple in theory. When a price difference emerges between two markets, traders should be able to buy in one location and sell in another, capturing the spread as profit.

For decades this logic has shaped how trading organizations think about arbitrage. If market prices are visible, spreads are detected quickly, and analytics systems process information fast enough, profitable opportunities should naturally follow.

Modern trading platforms already provide deep visibility into market prices across regions and time horizons. Traders can observe volatility, location spreads, and temporal dislocations in real time. Advanced analytics systems continuously scan markets for opportunities across hubs, delivery windows, and transportation routes.

Yet despite this technological progress, many arbitrage opportunities fail to translate into executed trades.

The reason is rarely a lack of market visibility. In most trading environments, spreads are clearly visible to traders and analysts. The real challenge lies elsewhere. Arbitrage fails not because prices are unknown, but because organizations cannot determine quickly enough whether a theoretical opportunity can actually be executed within the operational constraints that govern commodity movement.

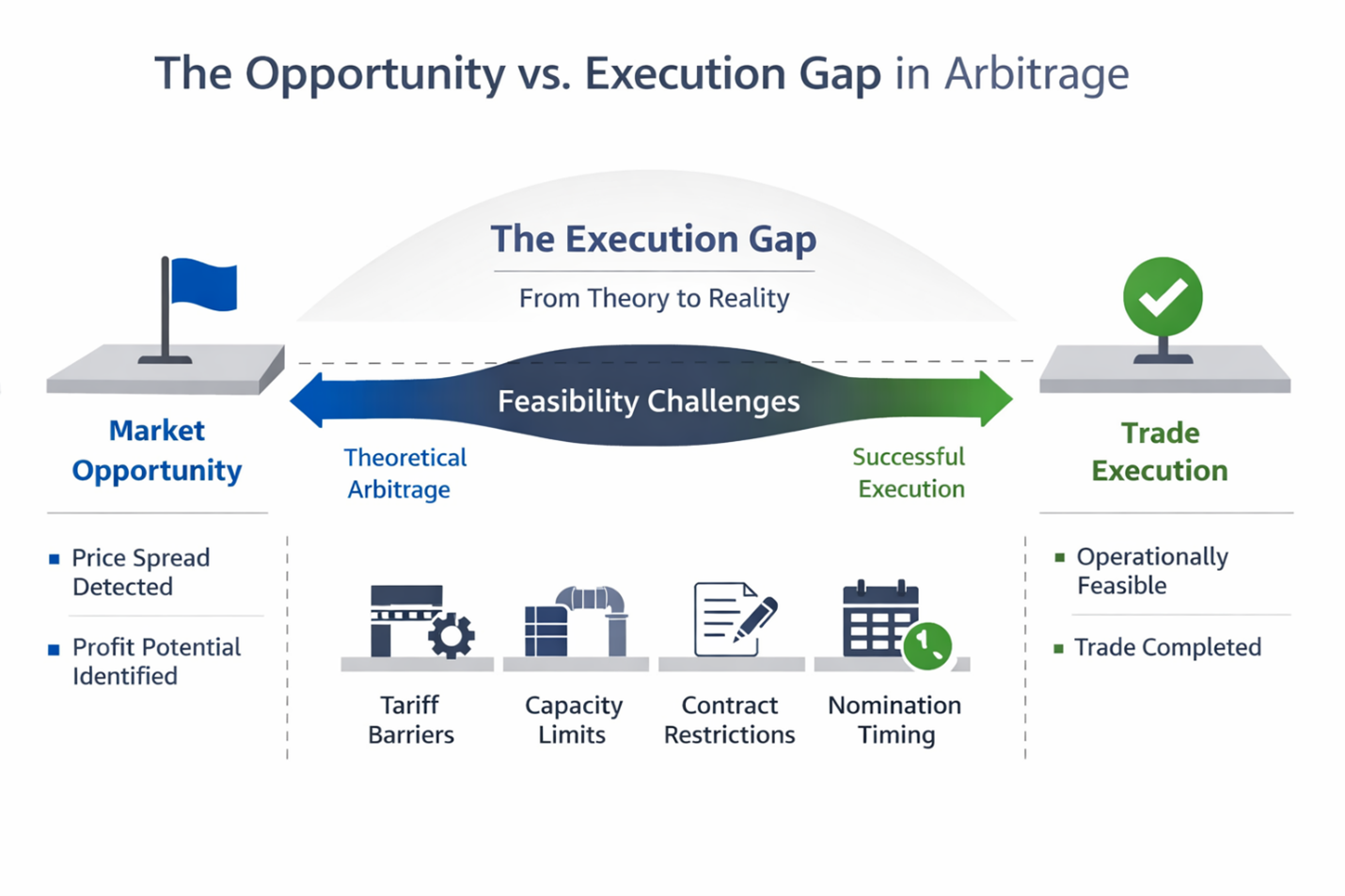

When Arbitrage Breaks Down It Is Rarely a Market Problem. It Is an Execution Problem.

The gap between opportunity and execution is where most arbitrage strategies break down. An arbitrage opportunity exists in theory, but execution exists in reality. Between these two states lies a complex network of operational constraints that determine what can actually happen in the physical world.

Tariff structures determine which movements across pipeline or logistics networks are permitted. Contracts define entitlements, obligations, and delivery rights. Infrastructure capacity determines what is physically possible across transportation networks. Nomination cycles define the operational time windows within which commodity movements can be scheduled.

In isolation these constraints may appear manageable. In practice they interact in complex ways across multiple operational systems.

Consider a simple example. A price spread may exist between two regional gas hubs. On paper the trade appears profitable. However, pipeline tariffs may restrict routing options, storage contracts may limit available volumes, and nomination cycles may delay scheduling until the next operational window. What appeared to be a clear opportunity may turn out to be operationally infeasible.

Because these constraints are fragmented across logistics systems, contractual documentation, tariff structures, and operational procedures, determining feasibility often requires extensive manual evaluation. By the time traders confirm whether the opportunity can actually be executed, the price spread may already have disappeared.

Arbitrage Decisions Are Slowed by Fragmented Operational Knowledge

Even in technologically advanced trading organizations, arbitrage evaluation often remains a manual process. The reason is not a lack of computational capability. The challenge lies in how operational knowledge is distributed.

Some constraints exist within infrastructure scheduling systems. Others are defined in tariff documentation or contract agreements. Many operational conditions exist only as institutional knowledge held by schedulers and operators who understand the behavior of infrastructure networks through experience.

Evaluating arbitrage opportunities therefore becomes an act of interpretation rather than calculation. Traders must translate pricing signals into operational feasibility by understanding how tariffs, routing constraints, contracts, and nomination schedules interact.

This fragmentation makes it difficult for traditional analytics platforms to automate the decision process effectively.

The Hidden Design Flaw Inside Most Arbitrage Systems

Another structural issue lies in how many trading analytics platforms are designed.

Traditional systems typically separate economic optimization from operational validation. The system first identifies profitable trades based purely on price spreads. Only afterward does it attempt to validate the opportunity against operational constraints such as tariffs, infrastructure capacity, contractual rights, and scheduling rules.

At first glance this architecture appears logical. In practice it introduces a fundamental flaw.

Operational constraints are not filters that should be applied after optimization. They are defining conditions that determine whether an opportunity exists in the first place.

When validation occurs after optimization, two types of errors commonly emerge. Systems recommend trades that cannot be executed in the real world, forcing traders to discard them after manual analysis. At the same time, potentially viable opportunities may be rejected because the system fails to consider alternative routing or scheduling options that could make the trade feasible.

Over time these inaccuracies erode trust in analytics platforms. Traders gradually return to manual judgment rather than relying on automated recommendations.

The Next Advantage in Energy Trading Will Come from Operational Intelligence, Not Faster Market Data

Many organizations attempt to solve arbitrage inefficiencies by investing in faster analytics systems and larger data platforms. While these investments improve the speed at which market data can be processed, they do not address the fundamental bottleneck in arbitrage execution.

The limitation is not computation. The limitation is operational interpretation.

Analytics systems may detect thousands of theoretical arbitrage opportunities within seconds. But without structured understanding of tariffs, contracts, routing constraints, infrastructure capacity, and nomination timing, each opportunity still requires manual validation.

A more effective approach embeds these operational constraints directly into the arbitrage discovery process.

Instead of identifying price spreads first and validating them later, modern arbitrage intelligence systems evaluate opportunities within the full operational context of the market. Pricing signals are analyzed alongside structured representations of transportation infrastructure, contract entitlements, tariff rules, routing possibilities, and nomination schedules.

When operational constraints are integrated into the discovery process itself, the opportunities surfaced by the system are already operationally feasible.

This dramatically reduces the time required to move from opportunity detection to trade execution.

From Market Signals to Executable Trades

Intelligent arbitrage detection platforms are beginning to apply this architecture within modern energy trading environments.

The Arbitrage Detection Agent developed by RandomTrees continuously evaluates market prices while simultaneously mapping operational feasibility across pipeline networks, storage infrastructure, and logistics routes. The system analyzes spreads across trading hubs while enforcing tariff structures, contractual entitlements, infrastructure capacity constraints, and nomination cycle requirements.

The platform automatically maps feasible transportation and storage routes across available infrastructure networks. It evaluates routing options and volume allocations to maximize arbitrage margins while ensuring compliance with operational constraints. Once feasible opportunities are identified, the system generates nomination ready execution plans that allow trading and scheduling teams to move rapidly from analysis to operational execution.

By embedding operational intelligence directly into arbitrage discovery, the platform ensures that opportunities surfaced by the system are not theoretical spreads but executable trades.

Organizations deploying such systems are seeing meaningful improvements in trading performance. Deal analysis that previously required hours of manual evaluation can now be completed within minutes. Decision to nomination cycles become significantly faster, allowing trading teams to respond to intraday price volatility more effectively.

Optimized routing and volume allocation also improve margin capture across transportation and storage networks.

The next wave of competitive advantage in energy and commodity trading will not come from seeing more prices or processing larger volumes of market data. It will come from understanding operational constraints earlier and more deeply within the decision process.

Markets move quickly, but operational systems move more slowly. The organizations that succeed will be those that align these two dynamics by embedding operational intelligence directly into trading decision frameworks.

This shift toward operationally aware arbitrage intelligence is exactly where modern trading systems are heading. RandomTrees developed the Arbitrage Detection Agent to address this gap by combining market analytics with structured operational reasoning across tariffs, contracts, infrastructure capacity, and nomination cycles. Instead of surfacing theoretical spreads that require manual validation, the platform identifies opportunities that are already operationally feasible and executable.

For trading organizations operating in increasingly volatile markets, this approach enables faster decisions, higher margin capture, and greater confidence in execution. As energy and commodity markets continue to evolve, platforms that unify market intelligence with operational constraints will define the next generation of trading infrastructure.

In arbitrage trading, the difference between seeing an opportunity and capturing it is rarely analytics. It is execution.